access to financial services & institutions

Having access to legitimate financial services is crucial during times of unemployment or employment uncertainty to provide immediate relief like government provided benefits, to manage existing funds and budgets, and to prepare for a financially sustainable future, considering any current or anticipated major life changes. It is important to expand financial access because nearly 10 million households in the U.S. are disproportionately unbanked. Without access to a bank or credit union, these individuals are not able to fully participate in local and national economics, and may be susceptible to pay for more financial services, theft and robbery due to keeping large sums of cash, facing challenges saving for emergency situations, struggle with building positive credit history, and lack of access to affordable credit for both short-term and long-term needs.

Financial Inclusion & Accessibility

What we know: According to The Brookings Institution,

-Women worldwide have less ability to broadly access the financial system than men.

-After controlling for income and education, women in developing economies are still more excluded from the financial sector than men.

-There is a gender gap in savings and credit behaviors.

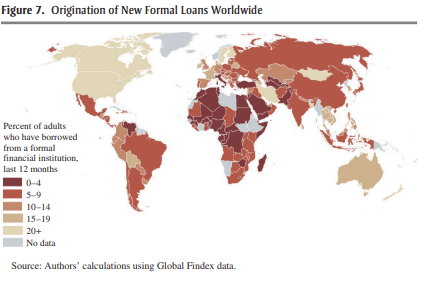

-In the US, over 25% of the poorest quintile has no access to a formal financial institution, compared to 9% in Canada, and 3% in the UK.

-More than 2.5 billion adults do not have formal financial accounts

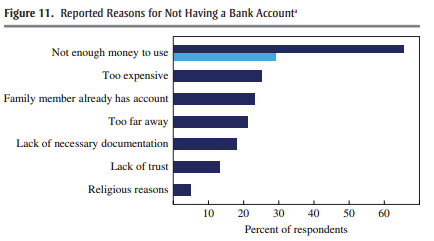

-Half of the adults around the world remain unbanked due to high costs, physical distance to a bank, and lack of proper documentation.

-A large percentage of the unbanked population could be included or have better access to the financial system through policy changes such as:

-Increased use of technology to minimize physical barriers

-Reduced withdrawal charges

-Relaxed documentation requirements

Determining access & measuring financial services

In 2024, the Treasury Office of Consumer Policy published the National Strategy for Financial Inclusion in the United States, based on data collected in 2023 and 2024.

-

The ability to fully and beneficially participate in the financial system is a foundation for household financial resilience, well-being, and opportunity to build wealth.

While the US has a robust financial infrastructure, this system does not work equally for all consumers.

There are disparities in how different populations interact with and benefit from financial products and services, particularly members of underserved and marginalized communities.

Improving inclusion in the financial system is critical to fostering financial resilience and well-being, and addressing wealth inequality in the US.

-

Many consumers do not access or participate in the public programs they may be eligible for and some programs are not funded sufficiently enough to serve all eligible Americans. Research estimates that only about 75% of eligible Americans participate in benefits they qualify for.

Key access challenges for consumers include time, effort, costs, complex forms to locate and complete, gathering necessary documentation, and navigating administrative processes. These burdens are often ongoing challenges for underserved consumers.

Many government financial products and services with specific requirements and features that create access barriers.

Government agencies may not effectively communicate what programs and credits are available, let alone how to navigate them.

Delivery mechanisms of these products and services imposing unwanted costs on recipients (Ex: fees to apply for benefits, file taxes, or access accounts)

-

Promote access to transaction accounts that meet consumer needs

Increase access to safe and affordable credit

Expand equitable access to savings and investments

Improve the inclusivity of financial products and services that are provided or backed by the government

Foster trust in the financial system by protecting consumers from illegal and predatory practices

-

Financial services provided to Americans’ by federal, state, local, and tribal governments can include entitlement programs, tax credits, credit products like loans and mortgages, and payment channels to disburse credits and payments.

Measuring the extent to which products and programs are successfully improving financial outcomes for consumers

Evaluate opportunities to expand on existing successes or refine design for greater positive impacts

Policymakers should review policies for income support programs to ensure they do not penalize those who are striving for financial stability, and utilize existing research to reduce unnecessary barriers to access

Federal policymakers should seek to learn from other public sectors, entities, or innovators in the private or nonprofit sector that seeks to advance financial inclusion

Financial inclusion is heavily influenced by how early individuals begin saving, investing, and building a credit history - policymakers should study how this impacts future financial inclusion and well-being when considering changes to federal policies

Federal and state agencies should work together to ensure that program administrators have appropriate information and resources for selecting vendors for government financial products and services that are designed inclusively and with consumer protection features that comply with applicable regulatory requirements.

Government agencies should take steps to simplify and streamline the processes by which individuals apply for or access government programs and payment

Government agencies should look for opportunities to enroll consumers in programs they may qualify for at existing consumer touchpoints

The US Department of Treasury encourages tracking of access, usage, and benefits of financial services, as well as holistic measures like financial well-being, financial resilience, or net worth. To assess the data regarding the state of financial inclusion, the federal government uses:

The FDIC’s National Survey of Unbanked and Underbanked Households

The Federal Reserve’s Survey of Household Economics and Decision-Making (SHED)

The Survey of Consumer Finances (SCF)

The CFPB’s Making Ends Meet survey

These surveys collect information about objective financial situations and subjective questions about how the household views their financial situation. It is important to note that the current measurements methods and research being done lacks information on financial exclusion barriers, and lacks specific demographic and regional information. Some stakeholders argue that household financial health metrics should be measured regularly, like other macroeconomic indicators such as gross domestic product and the unemployment rate.

variation in access by location

Changes in access to financial services and resources based on identity characteristics are not directly measured, but there are resources available to help determine disparities.

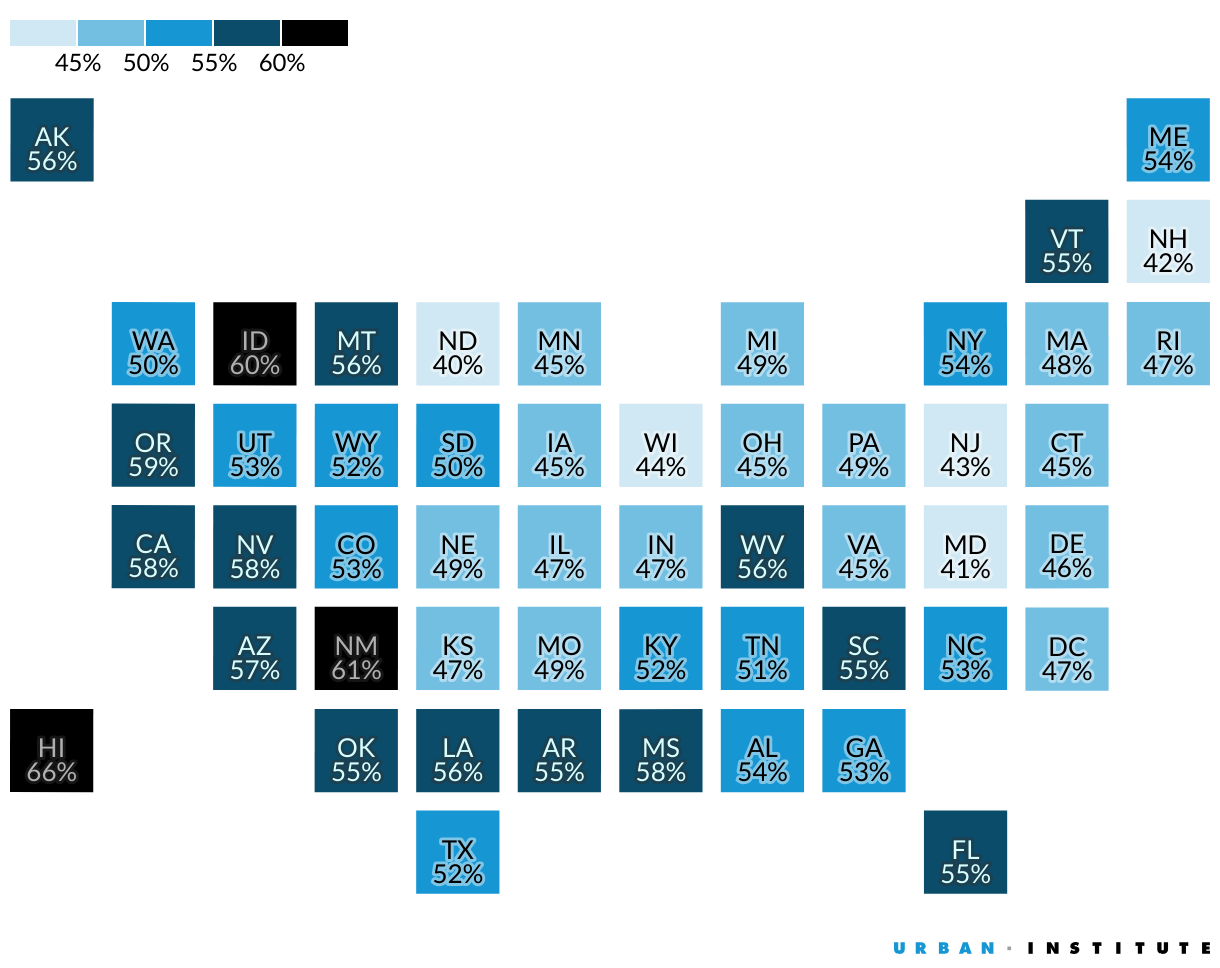

In 2025, a study was conducted to determine how many people in each US state have the financial resources to thrive. The study utilizes the True Cost of Economic Security (TCES) threshold to examine the share of people in families below the threshold by state, collecting information about objective financial situations and subjective questions about how the household views their financial situation. Using the TCES, we can determine that there are disparities in economic security and access to resources, but additional analysis is needed to better understand what is driving the disparities. To learn more about the TCES threshold, click here.

Possible causes for disparities according to the study include:

Reflected differences in the resources that families can access

Some states offering tax credits for working families, while other have expanded Medicaid coverage for adults

Economic opportunity, wage levels, and share of adults in the labor force vary by state, creating disparities based on location

Families in some states facing higher rent relative to household income or more costly childcare

Even in states with overall low costs, families in states with low resources AND low earning power may face the greatest challenges meeting TCES thresholds

The US Department of Treasury - Community Financial Access Pilot was designed to increase access to financial services and financial education to low-moderate income families and individuals, especially those lacking a credit union or a bank account. This project includes a mix of banks, credit unions, faith-based organizations, non-profits, credit counseling services, public agencies, educational organizations, and more, depending on location.

There are 8 locations who assumed the pilot project. Find information on Community Financial Access Pilot (CFAP) locations relevant to EPA Region 4 below:

If there is a location in your area, the corresponding community profile page provides an overview of the community’s financial issues, a strategy overview, and a list of partner organizations that individuals may contact for financial services or support

Variation in access by demographic

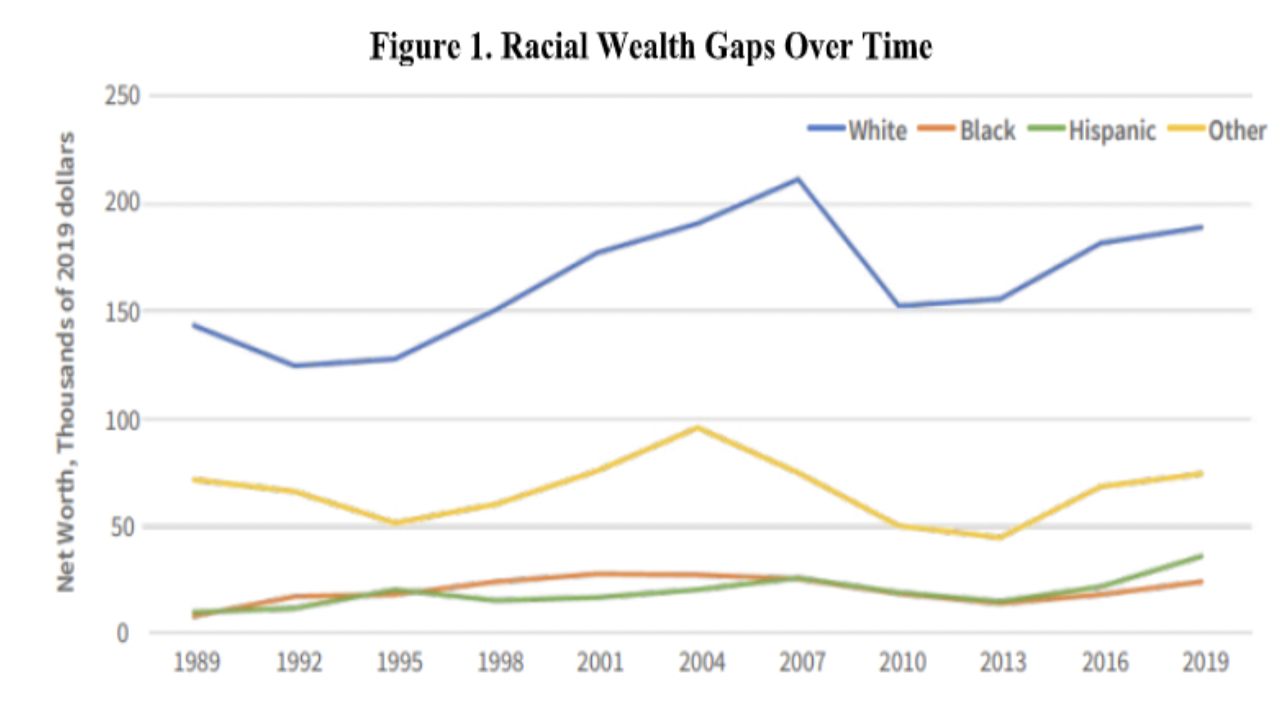

In 2022, the US Department of Treasury analyzed racial differences in economic security in the US.

-

The racial wealth gap is a key component to assessing economic security. Racial wealth gaps continue to persist, threatening the economic security of impacted families and weakening the economy as a whole.

Wealth is essential to economic security because it can be used for consumption, which is directly related to well-being. It is necessary for individual economic mobility and growth of the economy as a whole, and allows for the ability to take risks and become financially resilient.

Research indicates that there are long-lasting advantages of wealth accumulation in families:

Intergenerational wealth transfers

Gains in household wealth increase the probability that children enroll in and graduate from higher education, increasing their lifetime earning from employment

Low-wealth families are increasingly struggling to progress without wealth

Reduced physical and mental health

Lower survival rates

Affected health due to unaffordable healthcare

The median wealth gap between white and black families has hardly changed over the last 20 years.

Contributors to the racial wealth gap over time include racial differences in:

Home equity

Financial assets

Income

Research indicates that under current conditions, the racial wealth gap will continue to widen.

-

Structural solutions are necessary:

Policies that seek to reduce discrimination and bias in housing and labor markets

To better support households in times of financial distress

To decrease gaps in access to retirement accounts or liquid assets

Addressing racial differences in wealth will benefit all Americans.

Inequitable policies and practices that prevent wealth-building by some groups have been shown to negatively impact economic security for all.

Unequal societies are less likely to invest in public goods that enhance productivity, including education, infrastructure, public transportation, and technology.